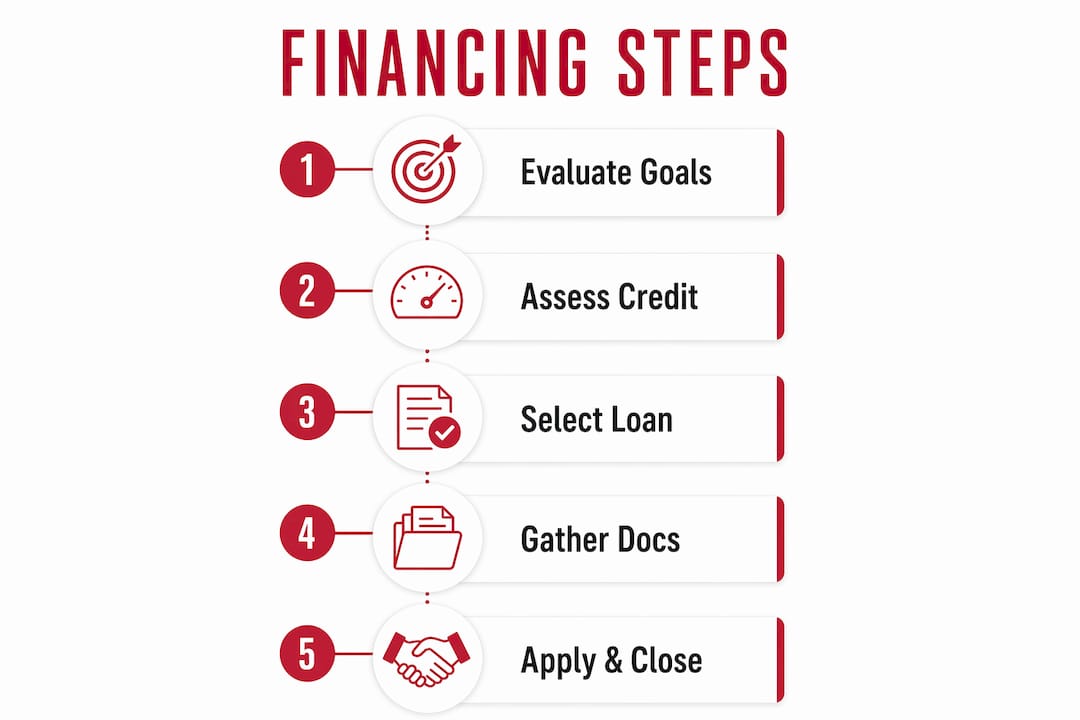

Financing luxury investment property means securing specialized mortgage products designed for high-value assets, where standard conforming loans simply do not apply. Jumbo loans, DSCR loans, and private bank financing each serve different investor profiles, and choosing the wrong structure costs more than a higher interest rate. The right loan aligns with your investment horizon, tax position, and portfolio liquidity. This guide breaks down every major option, the lender requirements you will face, and the expert strategies that separate competitive buyers from those who miss deals.

What are the main loan types for luxury investment properties?

Luxury property financing splits into four distinct categories, each with different qualification logic and cost structures. Understanding the differences before you approach a lender saves time and prevents costly missteps.

Jumbo loans are the most common vehicle for financing high-end real estate. These loans exceed the conforming loan limits set by Fannie Mae and Freddie Mac, which sit well below the price points of most luxury properties. Specialized jumbo loans allow down payments as low as 10% on properties over $2 million. That flexibility is a significant shift from the traditional 20–30% threshold most investors assume is fixed.

DSCR loans (Debt Service Coverage Ratio loans) qualify borrowers based on the property's cash flow, not the investor's personal income. DSCR loans require ratios of 1.0x to 1.25x, with interest rates starting around 6.0% and down payments of 20–25%. This structure is ideal for self-employed investors or those with complex tax returns that understate income. The lender looks at what the property earns, not what your W-2 says.

Portfolio loans come from banks and credit unions that hold the loan on their own books rather than selling it to the secondary market. This gives them flexibility to underwrite against your full financial picture. Private banks underwrite luxury mortgage loans based on holistic relationships, including total deposits and assets, enabling bespoke loan structures that do not appear on standard mortgage menus.

Bridge loans and SBLOCs (Securities-Backed Lines of Credit) serve investors who need speed or want to preserve portfolio exposure. Bridge loans close in 8–21 business days versus the 45–90 days conventional banks require. That speed is the difference between winning and losing a competitive offer in markets like La Jolla or Rancho Santa Fe.

| Loan Type | Down Payment | Qualifies On | Best For |

|---|---|---|---|

| Jumbo loan | 10–30% | Personal income and credit | Long-term holds, primary or investment |

| DSCR loan | 20–25% | Property cash flow | Self-employed, multi-property investors |

| Portfolio loan | Varies | Full financial relationship | Ultra-high-net-worth, complex profiles |

| Bridge loan | 30–35% (65–70% LTV) | Asset value and exit strategy | Fast closes, short-term holds |

| SBLOC | N/A (credit line) | Investment portfolio value | Liquidity preservation, avoiding asset sales |

Pro Tip: Request a pre-approval letter from your jumbo lender before you tour properties. Sellers in the $3M+ range routinely reject offers from buyers who cannot demonstrate financing readiness on day one.

How should you choose financing based on your investment goals?

The right loan structure depends on how long you plan to hold the property and what you want to do with your capital in the meantime. Long investment horizons of 10 or more years favor fixed-rate jumbo mortgages, while short horizons of 3–7 years favor variable-rate SBLOCs or bridge loans. Fixed rates eliminate interest rate risk over a decade. Variable structures cost less upfront when you plan to sell or refinance within a few years.

Tax position matters as much as rate. Mortgage structure choice impacts tax outcomes and long-term financial planning more than the nominal interest rate. An investor in a high tax bracket who sells appreciated securities to fund a down payment may trigger a capital gains event that wipes out years of rate savings. An SBLOC avoids that trigger entirely by borrowing against the portfolio without selling it.

Key decision factors to evaluate before choosing a loan structure:

- Investment duration. Holds under five years favor variable or bridge financing. Holds over ten years favor fixed jumbo loans.

- Income documentation. W-2 earners qualify more easily for jumbo loans. Self-employed investors often get better terms with DSCR loans.

- Portfolio liquidity. If selling assets to fund a down payment triggers capital gains, an SBLOC or bridge loan preserves your position.

- Estate and entity structure. Loans held in LLCs or trusts require different underwriting. Confirm your lender works with your entity type before applying.

- Rental income reliance. If the property's cash flow is central to your return model, a DSCR loan aligns the loan qualification with your actual investment thesis.

Pro Tip: Work with a CPA and a mortgage advisor simultaneously, not sequentially. The loan structure you choose in week one affects your tax return three years from now.

For investors building a long-term luxury portfolio, the financing structure is as important as the property itself. Getting this right at acquisition prevents costly refinancing later.

What do lenders actually require for luxury investment loans?

Lender requirements for luxury investment property loans are stricter than those for standard residential mortgages, and the documentation burden is higher. Lenders require strong DSCR ratios of 1.20 or above, higher reserves of 6–12 months, experienced borrowers, quality appraisals, and comprehensive insurance coverage. Meeting these benchmarks before you apply accelerates underwriting and signals credibility.

Credit score minimums typically range from 660 to 740 or above, depending on the loan type and lender. Jumbo loans from private banks may accept lower scores when the borrower's overall asset picture is strong. DSCR loans are more score-sensitive because the lender cannot offset risk with income documentation.

Reserve requirements are the most commonly underestimated hurdle. Lenders want to see 6–12 months of PITIA (principal, interest, taxes, insurance, and association dues) in liquid accounts after closing. On a $3 million property, that reserve requirement can exceed $150,000 in cash or near-cash assets. Investors who drain their accounts to fund the down payment often fail this test.

Appraisal standards for luxury properties are more complex than for standard homes. Comparable sales are scarce in high-value markets, and appraisers must often use properties from wider geographic areas or older time periods. A low appraisal on a $4 million property can kill a deal or force a larger down payment. Always hire an appraiser with documented experience in the specific luxury submarket.

Required documentation typically includes:

- Two years of personal and business tax returns

- Three months of bank and investment account statements

- Proof of rental income or signed lease agreements for DSCR loans

- Entity documents if purchasing through an LLC or trust

- A detailed insurance binder meeting lender minimums for high-value properties

What expert strategies prevent costly mistakes in luxury financing?

The single biggest mistake luxury investors make is approaching financing after they find a property. Successful luxury property investors prioritize pre-arranged financing facilities to move quickly in competitive markets. A pre-arranged bridge facility or private bank line lets you submit a clean offer without a financing contingency, which is a material advantage in markets where sellers receive multiple bids.

Overestimating rental income for DSCR qualification is a common and expensive error. Lenders use conservative income projections, often applying a vacancy factor of 10–25% to gross rental estimates. If your DSCR calculation depends on 100% occupancy at peak seasonal rates, the lender's underwriter will reject it. Build your projections on realistic stabilized occupancy before you apply.

SBLOCs preserve portfolio exposure while providing liquidity for property acquisition, avoiding capital gains realization. This is one of the most underused tools in luxury real estate financing. An investor with $2 million in a brokerage account can borrow against it at a low margin rate, fund a down payment, and keep the portfolio fully invested. The cost is the margin interest, which is often lower than a jumbo loan rate.

Ultra-high-net-worth investors typically avoid standard bank loans due to slow closing and rely on asset-backed bridges or private lending to secure trophy properties quickly. Conventional banks close in 45–90 days. Bridge loans close in 8–21 business days. In a market where a seller has three offers, the buyer who can close in two weeks wins.

Pro Tip: Assemble a team that includes a luxury real estate attorney, a CPA familiar with real estate tax law, and a lender who specializes in non-conforming loans before you make your first offer. Generic mortgage brokers rarely have access to the private bank products that matter most at the $3M+ price point.

Reviewing the 2026 luxury market report gives investors a clearer picture of where financing conditions and property values intersect in Southern California's most competitive submarkets.

Key Takeaways

Financing luxury investment property successfully requires matching your loan type to your investment horizon, tax position, and liquidity needs before you make an offer.

| Point | Details |

|---|---|

| Jumbo loans offer flexibility | Down payments as low as 10% are available on properties over $2 million with specialized jumbo products. |

| DSCR loans bypass income docs | Qualification based on property cash flow suits self-employed investors and multi-property portfolios. |

| Reserves are non-negotiable | Lenders require 6–12 months of PITIA in liquid assets after closing, often exceeding $150,000. |

| Speed wins competitive deals | Bridge loans close in 8–21 days versus 45–90 days for conventional banks, a decisive advantage. |

| Structure beats rate | Mortgage structure affects tax outcomes and portfolio liquidity more than the nominal interest rate. |

What I have learned financing luxury deals in Southern California

The investors I see succeed in this market are not the ones chasing the lowest rate. They are the ones who show up prepared. In over 15 years and more than $1.2 billion in transactions, the deals that fall apart almost always trace back to financing that was not arranged before the offer was written.

Private banking relationships change the game at the $3M+ level. A client with $10 million in assets at a private bank gets a phone call returned in hours, not days. That bank will structure a loan around the client's full financial picture, not a checklist. Standard lenders cannot do that. The investors who build those relationships before they need them are the ones who close the deals others miss.

The other shift I have seen is how investors think about debt itself. The old instinct was to minimize borrowing. The current reality is that mortgage debt is a liquidity tool, not just a financing necessity. Keeping capital deployed in higher-yielding investments while using tailored financing to acquire property is a wealth preservation strategy, not a shortcut. The investors who internalize that distinction make better decisions at every step.

My practical advice: start the financing conversation six months before you plan to buy. Get your documentation organized, establish the banking relationships, and know exactly which loan structure fits your goals. When the right property appears in La Jolla or Rancho Santa Fe, you will be ready to move in days, not weeks.

— Stu

How Stuharveyestates can help you find and finance your next property

Stuharveyestates brings over 15 years of experience and more than 250 completed luxury transactions to every client engagement in Southern California. When you are ready to act on a financing strategy, having the right property and the right guidance in the same place matters. Stuharveyestates provides access to curated listings across La Jolla, Rancho Santa Fe, Coronado, and the broader San Diego market, paired with expert coordination on financing structures and lender introductions. Browse current luxury property listings or connect directly with the buyers team to discuss your investment goals and the financing path that fits them.

FAQ

What is the minimum down payment for a luxury investment property loan?

Specialized jumbo loans allow down payments as low as 10% on properties over $2 million, though DSCR loans typically require 20–25%. The exact minimum depends on the loan type, lender, and borrower profile.

Can I qualify for a luxury investment loan without showing personal income?

Yes. DSCR loans qualify borrowers based on the property's rental income rather than personal tax returns, making them the standard choice for self-employed investors and those with multiple properties.

How many months of reserves do lenders require after closing?

Lenders typically require 6–12 months of PITIA in liquid reserves after closing on a luxury investment property. On a high-value property, this reserve requirement can easily exceed $150,000.

What is an SBLOC and why do luxury investors use it?

An SBLOC is a Securities-Backed Line of Credit that lets investors borrow against their investment portfolio without selling assets. It preserves portfolio exposure and avoids capital gains taxes while providing liquidity for a down payment or full purchase.

How fast can a luxury investment property deal close with bridge financing?

Bridge loans close in 8–21 business days, compared to 45–90 days for conventional bank financing. That speed gives investors a material advantage when competing for trophy properties in tight markets.