La Jolla property values remain strong because three structural forces reinforce each other: coastal land scarcity, regulatory limits on new construction, and a resident income base that sustains premium pricing regardless of broader market cycles. The average La Jolla home value sits at $2,343,961 as of May 2026, up 4.0% year over year. That figure is not a market anomaly. It reflects a community where supply cannot grow fast enough to meet demand, and where buyers have the financial capacity to compete at those levels. Understanding the specific mechanisms behind this stability is what separates informed investors from those who rely on gut instinct.

Why La Jolla property values remain strong: the core drivers

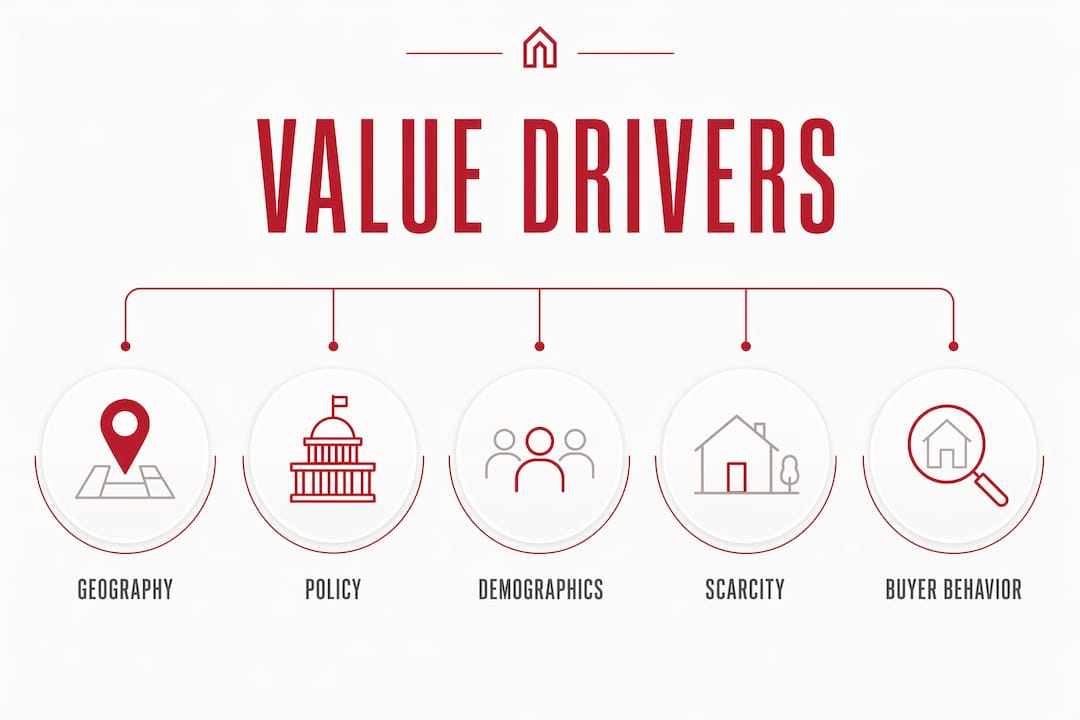

The three pillars supporting La Jolla real estate trends are geography, policy, and demographics. Each one independently limits supply or sustains demand. Together, they create a market that resists the corrections seen in less constrained coastal markets.

Geography sets the hard ceiling. La Jolla occupies a narrow coastal strip bounded by the Pacific Ocean to the west, Torrey Pines State Reserve to the north, and established urban development to the east. There is no undeveloped land waiting to absorb new housing. Every new unit competes for the same finite footprint, which keeps price per square foot elevated relative to inland San Diego neighborhoods where land is still available.

Policy reinforces what geography starts. Proposition D, passed in 1972, imposes a 30-foot coastal height limit west of Interstate 5. That single regulation prevents the kind of vertical density that has transformed other coastal cities. Without high-rise development as a release valve, housing supply stays tight and prices stay elevated.

Demographics complete the picture. La Jolla's median household income is $147,230, well above both the San Diego county and national medians. High local incomes mean the buyer pool can absorb price increases without demand collapsing. That income floor is one of the most underappreciated property value factors in La Jolla.

How land scarcity and coastal location drive pricing

Scarcity is the most direct explanation for La Jolla's price premium, and the data confirms it. April 2026 inventory shows 3.6 months of supply for single-family homes and just 2.5 months for condos and townhomes. Six months of supply is the conventional threshold for a balanced market. La Jolla sits well below that threshold, which structurally favors sellers and supports asking prices.

The coastal premium compounds the scarcity effect. Ocean views, beach access, and the microclimate that comes with a west-facing coastal location are attributes that cannot be replicated inland. Buyers who want those features have no substitute. That inelastic demand means price drops in the broader San Diego market rarely translate to equivalent drops in La Jolla.

Pro Tip: When evaluating a La Jolla property for investment, compare its price per square foot against the La Jolla average rather than the San Diego county average. County-level comparisons obscure the coastal premium and make La Jolla properties look overpriced when they are actually fairly valued for their submarket.

Here is how La Jolla's supply metrics compare to general market benchmarks:

| Metric | La Jolla (April 2026) | Balanced market benchmark |

|---|---|---|

| Single-family months of supply | 3.6 months | 6.0 months |

| Condo/townhome months of supply | 2.5 months | 6.0 months |

| Avg. single-family sale price | $3.895M | Varies by market |

| Avg. days on market | 54 days | 30 to 60 days |

Single-family homes in La Jolla sold at 95% of original asking price in April 2026, averaging $3.895M. That 95% figure signals that sellers are not capitulating on price. Buyers are meeting the market rather than forcing it down.

What zoning regulations do to long-term supply

Proposition D's coastal height restriction is not just a building code detail. It is the single most consequential policy shaping La Jolla's long-run supply curve. By capping structures at 30 feet in the coastal zone, the regulation prevents the density increases that would otherwise add meaningful housing stock over time. Policy constraints shape supply capacity more than individual market fluctuations, which stabilizes prices across cycles in La Jolla's coastal zone.

San Diego's Complete Communities initiative has attempted to incentivize density through bonus programs and streamlined permitting. La Jolla's community planning groups have resisted most density increases, citing neighborhood character and infrastructure capacity. That resistance is not unique to La Jolla, but it is particularly effective here because the regulatory baseline is already so restrictive.

Adaptive reuse of commercial and office space offers one alternative path to new housing units. Several projects have converted older La Jolla Village buildings into residential units without triggering height limit conflicts. These projects add supply at the margins but cannot offset the structural shortage created by decades of height restrictions.

"Regulatory limits such as Proposition D's coastal height restriction strongly influence the long-run supply curve and thus support resilient home values." — La Jolla housing density analysis

The practical implication for investors is straightforward. Regulatory constraints that limit supply do not disappear in down markets. A recession may slow transaction volume, but it does not add housing units. La Jolla's price floor has policy reinforcement that most markets lack.

How demographics and buyer behavior shape value stability

La Jolla's median household income of $147,230 creates a buyer pool with genuine purchasing power. That income level means demand does not evaporate when mortgage rates rise or when broader economic uncertainty increases. Buyers at this income tier absorb rate increases through larger down payments or cash purchases rather than exiting the market entirely.

Buyer behavior in 2026 has shifted in one important direction. Buyers are more selective about property condition, insurance costs, and HOA fees than they were in 2021 or 2022. This selectivity does not depress overall values. It concentrates demand on well-maintained, turnkey properties and creates a two-tier market where compromised inventory sits longer while quality homes move quickly.

For sellers, this means presentation and condition are now pricing variables, not just marketing considerations. A La Jolla home with deferred maintenance, high HOA fees, or unresolved insurance issues will trade at a discount even in a tight market. A turnkey property with ocean views and updated systems will attract multiple offers.

Pro Tip: If you are buying in La Jolla, request the full HOA financial statements and current insurance premium history before making an offer. These two data points now directly affect resale value and buyer pool size, especially for condos in the coastal zone.

The luxury segment adds another layer. Properties with panoramic ocean views, private pools, or direct beach access command premiums that track their own micro-supply. There are only a finite number of bluff-top lots in La Jolla. Demand for that specific inventory comes from a global buyer pool, not just San Diego residents, which insulates those properties from local economic fluctuations. You can explore the full range of La Jolla neighborhood options to understand how micro-location affects pricing within the community.

How La Jolla compares to surrounding San Diego markets

La Jolla outperforms the San Diego county median in cumulative home appreciation, driven by coastal premium and limited supply. That outperformance is not a recent trend. It reflects decades of constrained supply meeting sustained affluent demand. Investors who understand this dynamic treat La Jolla as a separate asset class from the broader San Diego market rather than a premium version of the same product.

Inland San Diego neighborhoods like Mira Mesa, Santee, and El Cajon have more developable land, lower price points, and buyer pools that are more sensitive to interest rate changes. When rates rise, those markets see faster price corrections because buyers have less financial cushion and more geographic alternatives. La Jolla buyers have fewer substitutes and more resources, which dampens price volatility.

| Factor | La Jolla | Inland San Diego |

|---|---|---|

| Avg. home value | $2.34M+ | $700K to $900K range |

| Months of supply | 3.6 (single-family) | 4 to 6 months |

| Primary buyer profile | Affluent, often cash or large down | Rate-sensitive, conventional financing |

| Long-term appreciation | Above county median | Tracks county median |

| New construction potential | Very limited | Moderate to high |

The Village and Shores districts within La Jolla itself show internal variation. The Village commands premiums for walkability and proximity to dining and retail. The Shores attracts buyers who prioritize beach access and a quieter residential feel. Both outperform inland markets, but understanding which micro-location aligns with your investment thesis matters when comparing specific properties.

For context on how La Jolla stacks up against other premium coastal communities in the region, the best luxury neighborhoods in San Diego analysis provides a useful benchmark across Del Mar, Rancho Santa Fe, and Coronado.

Key takeaways

La Jolla property values remain strong because coastal scarcity, Proposition D height limits, and a high-income buyer base create structural price support that persists across market cycles.

| Point | Details |

|---|---|

| Coastal scarcity drives pricing | Limited developable land and natural boundaries keep supply permanently constrained. |

| Proposition D limits new supply | The 30-foot coastal height limit prevents density increases that would otherwise add housing stock. |

| High incomes sustain demand | A median household income of $147,230 means buyers absorb rate increases rather than exit the market. |

| Buyer selectivity concentrates value | Turnkey, well-maintained homes hold value better as 2026 buyers scrutinize condition and costs. |

| La Jolla outperforms county trends | Cumulative appreciation exceeds the San Diego county median due to coastal premium and supply constraints. |

What 15 years in this market has taught me about La Jolla

Most buyers and investors I work with come to La Jolla having studied the county-level data. They know San Diego is a strong market. What surprises them is how little county trends actually predict what happens in La Jolla specifically.

I have watched La Jolla hold value during periods when inland San Diego corrected meaningfully. The reason is not mysterious. When you combine a hard geographic boundary, a 50-year-old height restriction, and a resident income base that is roughly double the county median, you get a market that behaves more like a trophy asset than a typical residential submarket. Trophy assets do not follow the same supply and demand curves as commodity housing.

The shift I am watching closely in 2026 is buyer selectivity. Clients are spending more time on due diligence than at any point in my career. Insurance costs in coastal California have become a genuine pricing variable. HOA reserve fund health is now a deal-breaker for some buyers, not just a footnote. This selectivity is actually healthy for long-term value. It means the properties that do sell are genuinely well-priced and well-maintained, which raises the quality floor for the entire market.

My practical advice for anyone targeting La Jolla right now: do not try to time the market based on rate movements. The structural factors that support values here are policy-driven and geographic. They do not change with the Fed funds rate. Buy the best property you can afford in the best micro-location you can access, and hold it. That strategy has outperformed every other approach I have seen in this market over 15 years.

— Stu

Find your La Jolla property with Stuharveyestates

Stuharveyestates brings more than 15 years of La Jolla market expertise and over $1.2 billion in completed transactions to every client relationship. Whether you are a first-time luxury buyer trying to understand micro-location pricing or an investor analyzing appreciation potential across the coastal zone, Stu Harvey's team provides the local knowledge and transaction experience to guide your decision with confidence.

The La Jolla market rewards buyers who move with precision and preparation. Stuharveyestates combines current market data with hands-on negotiation experience to position clients for the best possible outcome. Browse available La Jolla listings to see current inventory, or connect with the buyer support team for a personalized market consultation tailored to your goals.

FAQ

What is the average home value in La Jolla in 2026?

The average La Jolla home value is $2,343,961 as of May 2026, reflecting a 4.0% year-over-year increase. Single-family homes sold in April 2026 averaged $3.895M.

Why does La Jolla have so little housing inventory?

La Jolla's inventory stays tight because natural geographic boundaries limit developable land and Proposition D's 30-foot coastal height limit prevents new density. April 2026 data shows just 3.6 months of supply for single-family homes, well below the 6-month balanced market threshold.

Is La Jolla a good long-term real estate investment?

La Jolla has historically outperformed the San Diego county median in cumulative appreciation, driven by coastal scarcity and constrained supply. The structural factors supporting values, including geographic limits and regulatory restrictions, do not change with market cycles.

How does Proposition D affect La Jolla property values?

Proposition D sets a 30-foot height limit in La Jolla's coastal zone, preventing the vertical density that would otherwise add housing supply. This policy constraint has reinforced scarcity-driven pricing since 1972 and continues to shape the long-run supply curve.

What should buyers prioritize when purchasing in La Jolla in 2026?

Buyers in 2026 should prioritize property condition, current insurance costs, and HOA financial health before making an offer. Well-maintained turnkey properties hold value better and attract stronger buyer pools than compromised inventory, even in a tight market.